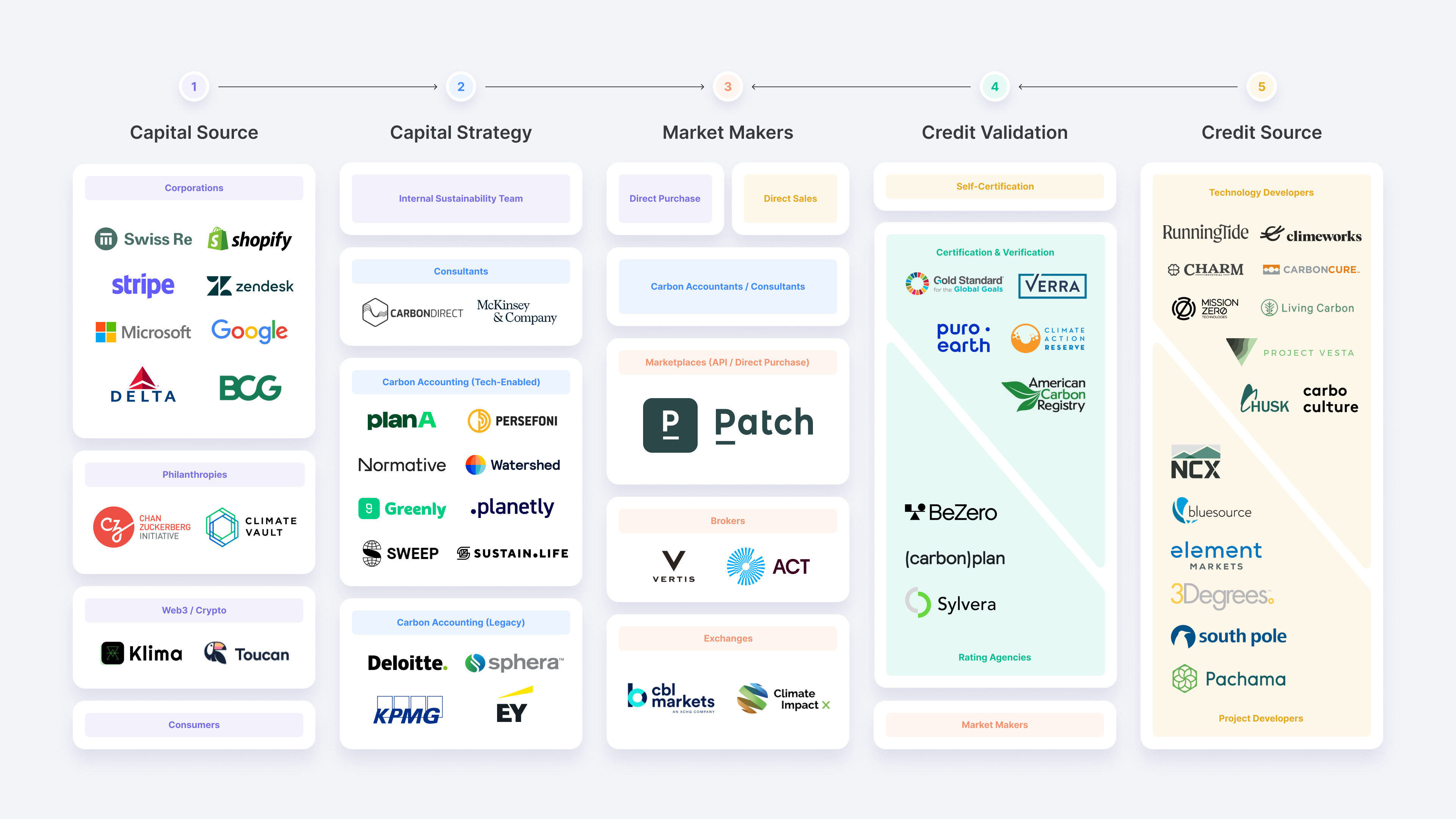

🏗️Patch and Building The Carbon Removal Economy

To finish our three-part series on carbon removal, I interviewed Ariel Hayward, the Sustainability Business Development Lead at Patch. Patch is a platform for negative emissions, meaning that it connects businesses looking to offset their carbon footprint with project developers focused on removing carbon from the atmosphere. Through our soil carbon program, Grassroots Carbon, we have seen how Patch can lead to sizable credit purchases, how they build custom interfaces for projects removing carbon, and how they facilitate the retirement of credits on behalf of purchasers. Patch has raised over $25M in venture capital funding to this end and is an instrumental startup in catalyzing the carbon removal economy.

Ariel’s background, from being a consultant at Bain to working on carbon strategy at Indigo Agriculture, creates a uniquely informed perspective on carbon markets and, in particular, agricultural carbon markets. She joined Patch because she “care[s] about [her] skillset making as much climate impact as possible. [She] wanted to take what [she] learned inhouse as a project developer into being a market maker with the end goal of making projects scale as quickly as possible.” Indeed, Patch is an “elegant way to allow project developers to focus on their core business” by supporting go-to-market strategy, delivery and quality risk mitigation, and buyer project portfolios management. I corresponded with Ariel about what it will take to create a reputable, accessible, and scalable carbon removal economy.

Patch’s Theory of Change

Kevin Silverman (KS): In 2021, the voluntary carbon market (VCM) scaled to over $1BN in transaction volume - a milestone that might end up looking minuscule if investors like Fred Wilson are right in saying that the VCM will reach $10BN by the end of the year. As more and more companies seek to buy credits to meet their publicly stated climate goals (such as agribusiness corporates), the opacity of the market is becoming increasingly cumbersome to buyers and project developers alike. Many non-profit and stakeholder groups have emerged to solve these issues, including McKinsey’s Taskforce For Scaling Voluntary Carbon Markets, the Integrity Council for the Voluntary Carbon Market (ICVMI), and the Voluntary Carbon Market Integrity Initiative (VCMI) (creative naming, I know). In particular, the McKinsey report mentions how “Today’s voluntary carbon market lacks the liquidity necessary for efficient trading, in part because carbon credits are highly heterogeneous.”

I find unparalleled value in the work of startups like Patch that can move as quickly as necessary to meet growing demand, unburdened by stakeholder and bureaucratic engagement. What is Patch’s theory of change?

Ariel Hayward (AH): The need for rapid decarbonization and carbon removal is clear. We need all solutions to be scaled as soon as possible to avoid the worst climate outcomes. Patch delivers the infrastructure to accelerate the climate solutions needed by delivering efficiency and liquidity to carbon markets by connecting buyers and sellers of carbon credits.

By building infrastructure for and moving credits on behalf of project developers, Patch allows project developers to focus their resources on carbon removal and avoidance and less of their energy on the administrative work of running a climate business.

This model also makes corporate climate action easier. The Patch platform allows businesses of all sizes, across industries, to easily contribute to project developers through the purchase of credits.

As Ariel pointed out during our conversation, the carbon markets “are a market that looks like a market, but it isn't necessarily anyone’s narrow self-interest.” Thinkers like Mark Tercek make great arguments as to why it is in a company’s best interest to go green and, if necessary, buy offsets. Ariel brought up an interesting framework for thinking about carbon credits: the problem of the Tragedy of the Commons.

Historically, if a company has grown based on extracting a shared natural resource, depletion occurs without coordination to sustain that resource and the enabling environment. The same may be true with tackling carbon emission effectively: as “the rules of the carbon world are still being written”, creating a pathway for collaborative, active investment in climate solutions is the key approach. In a voluntary, non-government regulated market, this becomes all the more complex. Creating a shared vocabulary would allow for equivalencies across carbon credit project types - and their co-benefits. Indeed, methodologies to generate credits still need iterations - it’s a necessarily messy process. Working with buyers, public officials, startups, and other stakeholders accepting innovation cycles, and learning by doing is key.

KS: What levers need to be pulled to grow carbon credit volumes and make a climate impact?

AH: There are several key levers. The top few I see are:

Investment in early stage approaches to carbon crediting - both academic and commercial funding: Many of the solutions that will have a massive positive impact on the climate are in their infancy, meaning they need capital at the academic and early commercial stages to scale.

Measurement, reporting and verification (MRV) innovation: Increasing the ease and efficiency with which we can measure, report and accurately verify climate outcomes from carbon credit projects is critical to crowding more investment and more credits into the space. Buyers need to be certain that the credit they buy represents a real tonne of carbon avoided or removed from the atmosphere, so MRV innovation needs to keep pace with technological innovation.

Continued evolution in the standards and accounting treatment of carbon credits: Given corporates are the most significant buyer by volume of voluntary carbon credits, clarity in both the specifications of each carbon credit and the accounting treatment of credits is critical. Clear global guidance around (a) what constitutes a high quality carbon credit? and (b) what types of claims do corporates get to make using different types of carbon credits? is vital.

Demonstrated demand for carbon credits: Forward purchase agreements and other commitments to the purchase of carbon credits are vital to project developers’ ability to raise capital required to expand production.

What’s the Deal With Soil Carbon Credits?

KS: Given this newsletter’s focus on regenerative agriculture and Ariel’s background in developing regenerative carbon projects, the future of soil carbon markets merits a deeper dive. So, what’s the deal with agricultural credits? The soil carbon market, as we have previously touched on at The Regeneration Weekly, is scaling quickly, but what are the barriers to getting it right?

AH: Broadly speaking, there are a few primary barriers to scaling SOC credits:

Grower / producer adoption: Having more growers recognize the value of generating SOC credits, both to the health of their fields and to their own financial bottom line, is the key driver. Further, growers will need easy ways to provide the required data regarding their management practices.

Price: Price per tonne and tonnes per acre/hectare are the factors that determine the ROI for the grower/producer. As such, price and performance are major drivers of grower adoption → SOC credit production.

Agronomic Calendar: The transition to soil health practices does not happen overnight. Instead, it often takes many agronomic cycles to reach full SOC potential through soil health practices. Therefore, even when a grower/producer decides to make the shift, it still takes time to create credits from that shift.

Models and soil samples: Production of soil carbon credits requires both detailed biogeochemical modeling and soil sampling. In many parts of the world, the literature / datasets are not yet robust enough to calculate / verify credit volume. Additionally, soil sampling is costly, which is one of the reasons sample-only approaches have historically had a difficult time scaling. Modelable domain expansion and cheaper soil sampling represent major unlocks in this space.

KS: Many of those problems will be solved with all the talent tackling the soil carbon measurement bottleneck, while a higher price of carbon will lead to both producer interest and better unit economics. However, fitting agriculture into carbon crediting isn’t always the cleanest. This is because traditional carbon credits typically took land out of production. So, to account for the additionality and permanence in working lands with active production cycles in carbon crediting schemes, what do you suggest?

AH: Additionality describes measures that would not have been taken but for a carbon credit requirement. In forestry and agriculture it will continue to be important to determine that projects generating carbon credits - SOC, afforestation, and reforestation projects - would not have happened without the potential sale of carbon credits. And permanence is the measure of how long the carbon will remain out of the atmosphere. Due to natural cycles and events like forest fires, there are continuing discussions about how best to measure the volume of carbon credits generated from both approaches. One approach is to include a 'buffer' of carbon sequestered to accommodate for potential loss from these natural events. I believe questions of additionality and permanence will continue to be discussed, specifically for agriculture, and I look forward to continuing to be part of the conversation.

In our conversation, thinking of production-based carbon credits as a “portfolio-wide” solution also helps assure performance and appropriately accounts for individual decision-making. Overall, this will help lead to a system-wide change where carbon credit income directly influences a grower’s yearly decision-making. With this, agricultural credits will grow in standardized value and create a “shared vernacular across credit types.”

Future of Carbon Markets

To end, I asked Ariel about the carbon market to come.

KS: What are your thoughts on Direct Air Capture (DAC) and other engineered removal vs Nature-Based Solutions?

AH: We need all of the solutions we can get and as fast as possible. Full stop. That said, we need to be conscious of scale potential now vs. in the future, and how we can most efficiently unlock investment to scale frontier solutions (DAC/engineered and NBS both). Natural systems have significant near-term climate impact potential. But they cannot solve the problem alone. We also need to be investing in chemical and mechanical solutions. Patch’s mission is to “Enable gigatonne scale carbon removal” - and to do that we are focused on creating the infrastructure to enable the expansion of all potential carbon removal solutions.

KS: Any thoughts on how co-benefits will scale? Should it remain as an add-on to carbon credits (and built into prices) or become parallel markets?

AH: In my opinion, it will depend on the demand. Does a buyer in the voluntary market prefer to purchase co-benefits separately? Or continue to keep them bundled? How are these co-benefits certified? By whom? To what end? At this point in the evolution in the market, I see co-benefits continuing to be bundled with carbon credits in the near-term, and I believe it's too early to know decidedly whether that will be the long-term path.

KS: What's the biggest risk in your opinion to scaling carbon markets?

AH: Quality and clarity. A carbon credit is unlike any other commodity available on the market today - you cannot take physical possession of the carbon. In fact, you're paying to get rid of the carbon or avoid it in the first place. Because of this, certainty that the credit is real is paramount. The continued evolution of MRV will provide more certainty to buyers - which is critical to ensuring buyers have the assurance they need that they are creating real climate impact. Similarly, clarity around credit attributes (additionality, permanence, leakage, etc.) will help us come up with the equivalent of a "spec sheet" for different types of credits. All of these components are absolutely critical to scaling carbon markets - the buyer has to know what they're buying and have confidence in it.

KS: If you had a magic wand to invest $100M in the carbon market infrastructure, what would you invest in?

AH: MRV across all project types, such that buyers have the confidence they need to funnel several multiples of that $100M into carbon projects.

Thanks to Ariel for the insightful and thought-provoking conversation. I highly encourage you all to onboard your company on Patch and check out their carbon credit offerings - and if you’re a project developer, get your project listed!

Disclaimer: The Regeneration Weekly receives no compensation or kickbacks for brand features - we are simply showcasing great new regenerative products.

If you have any products you would like to see featured, please respond to this newsletter or send an email to Kevin(at)soilworksnaturalcapital.com

The Regeneration is brought to you by Wholesome Meats | Soilworks | Grassroots Carbon| Grazing Lands